Credit for agri-food systems

On February 4, Standard & Poor’s (S&P) released the credit ratings for the World Bank’s bonds using a new methodology approved in October 2025. This methodology emerged after long discussions between the credit rating agencies—Moody’s and Fitch, in addition to S&P—and the multilateral development banks (MDBs). Those discussions began in the aftermath of the 2008–2009 global financial crisis. More recently, the issue gained renewed attention through the work of the G20 on strengthening the role of MDBs, particularly through efforts “to optimize their balance sheet.”[1] In practical terms, balance-sheet optimization means finding ways for MDBs to lend more and mobilize additional private capital without requiring member countries to contribute more public funds to increase what is known as the banks’ paid-in capital.

|

“New rating methodologies could unlock USD 600–800 billion in additional MDB lending over the next decade—without more public capital” |

S&P’s new methodology addresses **some—but not all—** of the proposals discussed in the G20 process.[2] Its application could allow MDBs to expand lending while maintaining their current capital base and preserving their AAA (or near-AAA) credit rating under S&P’s assessment. Moody’s and Fitch are still using their previous methodologies.

Maintaining those high credit ratings is critical. It allows MDBs to borrow at very low interest rates in international financial markets through the bonds they issue. These lower borrowing costs can then be passed on—after covering operational costs and other expenses—to member countries that borrow from the banks. According to S&P estimates, the methodological changes could allow the main MDBs to expand their loan and investment portfolios by around USD 600-800 billion over a decade.[3]

|

“High credit ratings allow MDBs to borrow cheaply in global markets and pass those lower costs to borrowing countries.” |

To put this figure into context: the total development loan portfolio and related assets of the five largest MDBs was approximately USD 1 trillion in 2024–2025.[4] Importantly, the additional USD 600–800 billion refers to an increase in the stock of loans and development assets on MDB balance sheets, not to an equivalent increase in annual lending flows.

How did S&P open the door to this potential expansion?

The answer lies in two key concepts:

- Preferred Creditor Treatment (PCT).

- Callable capital (CC).

Understanding these concepts is essential because they affect how rating agencies evaluate the risks associated with MDB lending to developing countries, and therefore the risks faced by investors who purchase MDB bonds.

Before explaining these concepts in detail, allow me a small personal note. While serving as Executive Director on the Board of the Inter-American Development Bank between 2003 and 2012, I participated in many discussions on these issues. So, allow me a moderate victory lap while revisiting those debates in what follows.

The structure of MDB capital

The financial structure of MDBs dates back to the Inter-American Bank created in 1940[5] whose model was later adopted by the World Bank in 1945 and subsequently by other MDBs. The subscribed capital of these institutions consists of two components:

- Paid-in capital – funds that member countries actually contribute in cash.

- Callable capital – a guarantee from member countries that can be “called” if necessary to ensure the bank can meet its obligations to bondholders.

Paid-in capital, together with retained earnings from MDB operations, forms the institutions’ equity capital. This equity is a key variable in several financial risk indicators used to evaluate the banks’ financial health.

Two important ratios are commonly used:

- Debt-to-capital ratio, which reflects the borrowing side of the balance sheet.

- Development assets-to-capital ratio, which reflects the lending and investment side.

The capital required to ensure repayment of the banks’ debt is linked to the risk of non-repayment associated with their loans and investments.

Preferred creditor treatment

Another important feature of the MDB system is preferred creditor treatment (PCT).

In practice, borrowing countries typically give priority to repaying debts owed to MDBs (and the IMF) over other external obligations. Even in difficult financial situations, countries tend to maintain payments to these institutions.

Together, PCT and callable capital—along with other safeguards such as liquidity requirements—help ensure that MDB bondholders are repaid on time. These protections are a fundamental reason why MDBs enjoy AAA or near-AAA credit ratings.

Those high ratings allow MDBs to borrow in global financial markets at lower interest rates than most of their member countries could obtain on their own, making development lending cheaper.

Why were these factors historically undervalued?

|

“For years, credit rating methodologies did not fully account for key safeguards that reduce MDB lending risks.” |

Despite their importance, credit rating agencies traditionally did not give full weight to PCT and callable capital when assessing MDB creditworthiness. Their reasoning was twofold:

- Preferred creditor treatment is not formally codified in international law; it is a long-standing practice rather than a legally enforceable rule.

- Callable capital, although clearly established in MDB founding agreements, has rarely been used, which led some analysts to question how easily it could be mobilized in practice.

As a result, the rating agencies tended to underestimate how much these two features reduce the risk faced by MDB as lenders and investors and, therefore, the risk of non-payment to those holding MDB’s bonds .

The consequence was that MDBs were often more constrained in their lending than necessary, because their lending capacity was assessed using a more conservative view of risk than the institutions’ actual financial structure might justify.

|

“Recognizing PCT and callable capital can significantly expand MDB lending capacity with the same capital base.” |

A numerical example

Consider a simple example:

Suppose that, without taking preferred creditor treatment (PCT) and callable capital (CC) into account, the risk of MDB operations requires 100 units of capital to support 300 units of lending to developing countries. This implies a leverage ratio of 3 (300/100).

Now assume that PCT and CC are fully considered in the risk assessment. In that case, the same 300 units of lending might require only 70 units of capital to cover potential repayment risks. This implies a leverage ratio of 4.29 (300/70).

Under this scenario, MDBs would have 30 units of capital freed up (100 minus 70). If the same leverage ratio were applied, those 30 units could support about 129 additional units of lending or investments.

It is important to note that the 129 units represent a stock, not an immediate flow of lending. Reaching that level would require a gradual increase in lending over time, depending on operational and financial factors.

Source: Photo by Arturo Añez on Unsplash.

During my time as Executive Director on the Board of the Inter-American Development Bank (IDB)—and on several occasions Chair of the Board’s Budget and Financial Policies Committee—I repeatedly argued that PCT and CC were not being properly valued, which unnecessarily constrained the lending capacity of the Bank.

My argument was that credit rating agencies misunderstood the nature of MDBs. Borrowing member countries are not simply “clients”; they are shareholders. This point was often emphasized by Enrique Iglesias, then President of the IDB. In that sense, the traditional distinction between “donors” and “recipients” is misleading. All member countries are partners and shareholders, with responsibilities as owners of the institution.

|

“In MDBs, borrowing countries are not just clients—they are also shareholders.” |

However, the risks associated with borrowing countries were often assessed as if they were clients in private financial markets, using their credit ratings with private creditors as a proxy. That relationship is fundamentally different.

If a country is a shareholder in a major international financial institution, its government will think carefully before taking actions that could damage that institution—particularly when it has capital invested in it[6] and relies on it as a key source of accessible financing[7].

Being both borrowers and shareholders also means that developing countries have a strong interest in two things: ensuring the effectiveness of development operations—because they must repay the loans—and preserving the financial strength of the bank, which provides them with access to affordable financing and potentially more impactful development programs.[8]

There is also a more informal but still important factor. If a country were to default or otherwise undermine the financial strength of an MDB, the minister representing that country on the Board of Governors, and the country’s representative on the Board of Executive Directors, would likely face a significant degree of “shame and blame” from other shareholders, especially from fellow borrowing countries.

Those countries might see their own financial costs increase because of such behavior.

Having participated in many MDB annual meetings, I can also attest that ministers and officials from developing countries value these gatherings highly. They do not want to arrive at those meetings only to face complaints that their country’s actions are harming the institution and its members.

Finally, if callable capital ever had to be activated, the founding charters of MDBs require that all shareholders contribute in proportion to their shares—not only the traditional “donor” countries with AAA credit ratings.

I recall discussing these issues frequently with colleagues responsible for finance and risk analysis. Some of them argued—often citing the views of the rating agencies—that there were not enough observations of defaults to estimate risks quantitatively with confidence.

My response was always that the absence of defaults was itself a very strong data point.

In any case, the global financial crisis of 2008–2009 made these discussions even more urgent. At the IDB, I suggested—and the proposal was accepted—to increase callable capital temporarily through an allocation generously provided by Canada. This allowed the Bank to expand lending during the crisis, before a formal capital increase was approved in 2010.

After the crisis, discussions between MDBs and credit rating agencies about how to properly measure risk intensified, encouraged in part by the work of the G20.[9]

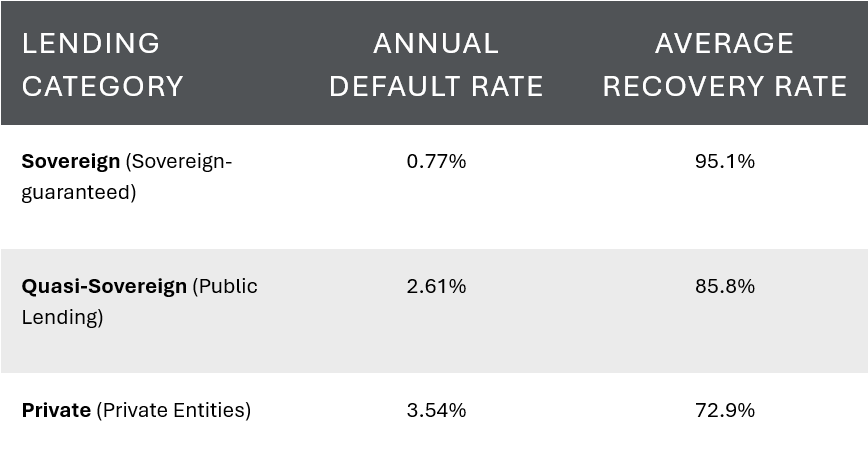

One important outcome of these efforts was the creation in 2009 of the Global Emerging Markets Risk Database (GEMs), initially launched by the European Investment Bank and the International Finance Corporation (IFC). Today, the initiative includes 26 international financial institutions, which contribute data on defaults and recovery rates.

|

“Three decades of data show very low default rates and high recovery rates in MDB operations.” |

Data published in 2024, covering the period 1994–2024, show very low default rates and high recovery rates. This pattern applies not only to sovereign lending (loans guaranteed by governments), but also to quasi-sovereign borrowers—such as provinces or state-owned enterprises—and even to private companies without government guarantees.

Source: Global Emerging Markets Risks database (https://www.gemsriskdatabase.org/)

In the database:

- The annual default rate is calculated as the number of countries or entities in default divided by the number with active operations in a given year (expressed as a percentage).

- The average recovery rate measures how much of the defaulted loan or investment is recovered—expressed in present value of principal and interest—relative to the outstanding amount at the time of default.[10]

If one assumes that the frequency of defaults is roughly proportional to their value within the portfolio[11] and considers the recovery rates shown in the table, the estimated average annual losses would be approximately:

- 0.038% for sovereign lending.

- 0.371% for quasi-sovereign lending.

- 0.959% for private sector operations.

An interesting observation is that preferred creditor treatment formally applies only to sovereign-guaranteed operations, yet its protective effects seem to extend even to private sector lending without government guarantees.

This likely reflects the fact that borrowing countries are also shareholders of MDBs. Private-sector operations typically require government notification and a formal “non-objection.”

|

“MDB safeguards appear to protect not only sovereign loans but also private-sector operations.” |

Moreover, through their participation in MDB governing boards, governments are informed about potential problems with private-sector projects and have various ways to monitor those operations to ensure they do not jeopardize the institution’s credit standing.

S&P has argued that its new methodology—which gives greater weight to PCT and CC when assessing MDB risk—is possible today because more systematic data are now available, demonstrating the historically low default rates and high recovery rates reflected in the GEMs database.

In my view, much of this information was always available in the financial statements of MDBs, although it had not been harmonized or compiled in a single database. In other words, the suggestions I was making two decades ago could have been implemented earlier.

Still, it is encouraging that these changes have finally taken place. Hopefully Moody’s and Fitch will follow the same path.

An additional benefit of the GEMs database becoming public is that other financial institutions have begun using it to design mechanisms that expand MDB lending without requiring additional paid-in capital. Examples include risk-transfer and credit-guarantee operations, such as the Room2Run initiative of the African Development Bank[12], as well as similar initiatives developed by the Asian Development Bank, IFC, and IDB Invest (the private-sector arm of the Inter-American Development Bank).

Challenges and opportunities

A key challenge now is to help developing countries build a strong pipeline of projects capable of using this expanded lending capacity.

It is important to remember that MDBs do not determine their lending programs on their own. Projects and programs must be designed jointly with the borrowing countries.

In the case of agri-food systems, preparing such projects requires specialized technical capacity. Organizations such as IICA, the CGIAR centers, and others can play an important role in helping governments, farmers, and private-sector actors design programs that are technically sound and ready for financing.

|

|

🖋️ About the author Eugenio Díaz-Bonilla, Special Advisor, Inter American Institute for Cooperation on Agriculture (IICA). Senior Visiting Research Fellow, IICA/IFPRI program. |

BlogIICA Editorial Committee

- Joaquín Arias Segura, Coordinator of OPSAA, IICA.

- Eugenia Salazar, Economist, OPSA, IICA

*The opinions expressed in this blog are those of the author and do not necessarily reflect the views of IICA or its member countries.

Notes

1. Boosting MDBs’ Investing Capacity: An Independent Review of Multilateral Development Banks’ Capital Adequacy Frameworks (2021) https://www.dt.mef.gov.it/export/sites/sitodt/modules/documenti_it/news/news/CAF-Review-Report.pdf ; G20 Roadmap for the Implementation of the Recommendations of the G20 Independent Review of MDBs’ Capital Adequacy Frameworks (2023) https://cdn.gihub.org/umbraco/media/5355/g20_roadmap_for_mdbcaf.pdf; and the two reports of the G20 Independent Expert Group https://www.cgdev.org/sites/default/files/The_Triple_Agenda_G20-IEG_Report_Volume1_2023.pdf; G20 Roadmap Towards Better, Bigger And More Effective MDBs (2024). https://coebank.org/documents/1724/G20_Roadmap_towards_better_bigger_and_more_effective_MDBs_T69DXmX.pdf ↩

2. The G20 Independent Expert Group (IEG) suggested lowering equity/debt leverage ratios, better accounting for “callable capital” in risk assessments, using innovative Instruments, such as hybrid capital, and risk transfers and guarantees. ↩

3. There are other possible changes in motion, as mentioned in the previous footnote, which may increase the potential loan portfolio even further, without having to increase the “paid-in” capital. ↩

4. World Bank Group (IBRD, IDA and IFC), some USD 570 billion; Asian Development Bank, about USD 160 billion; Inter-American Development Bank Group, some USD 150 billion; African Development Bank, some 40 billion; and the non-EU part of the European Investment Bank, some USD 80 billion. ↩

5. See Díaz-Bonilla and del Campo, 2010. A Long and Winding Road: the Creation of the Inter American Development Bank. https://www.amazon.com/Long-Winding-Road-Creation-Development/dp/1257089994. ↩

6. I argued that the real exposure of the bank in a country should be net of the capital invested in the bank. ↩

7. And even without cutting full access to lending, the annual lending program could be scaled down if the borrowing member country was endangering financial or other aspects of the operation of the bank. ↩

8. Another financial issue that I argued against is the practice of valuing guarantees issued by the bank to sovereign countries at 100% of the nominal value of exposure, and not at the potential value at risk. Later, this was one of the recommendations of the G20 reform for MDBs. ↩

9. I left the IADB in early 2012, so I was not direct part of what followed. ↩

10. The nominal value of capital and interests may have been recovered entirely, but because it happened later than the time when it should have been collected, the present value at the moment of recovery is utilized. ↩

11. As usually are the smaller countries that default, this would exaggerate the value impact on the portfolio. ↩

12. See https://www.afdb.org/en/news-and-events/african-development-bank-and-partners-innovative-room2run-securitization-will-be-a-model-for-global-lenders-18571; and, among others, https://www.afdb.org/sites/default/files/documents/balance_sheet_otimization_r2rs.pdf ↩

Add new comment